India is attempting something no country has done: build 50 GW of pumped storage hydropower in less than a decade.

The scale is staggering. From approximately 4.7 GW operational today, the target is 51 GW allocated across 39 projects by 2032, and the CEA roadmap extends to 100 GW by 2035-36. The investment: Rs 5-6 lakh crore. The justification: India’s renewable energy capacity is growing at one of the fastest rates in the world, and without grid-scale energy storage, the intermittent solar and wind generation cannot be reliably integrated.

Pumped storage is the answer. At 189 GW globally and providing over 90% of grid-scale energy storage, it is proven, scalable, and has a 50+ year lifespan that battery systems cannot match. India’s 267 GW of identified potential confirms the geography supports it.

But there is a question that the policy papers, investment announcements, and project allocation orders do not address: is India’s concrete technology infrastructure ready to deliver this buildout?

The Pipeline: Project by Project

Operational (approximately 4.7 GW)

| Project | State | Capacity | Status |

|---|---|---|---|

| Nagarjuna Sagar | Telangana | 705.6 MW | India’s first PSP (1980-85) |

| Srisailam LBPH | Telangana | 900 MW | Operational |

| Purulia | West Bengal | 900 MW | Commissioned 2007 |

| Sardar Sarovar | Gujarat | 1,200 MW | Not operating in pumping mode |

| Kadamparai | Tamil Nadu | 400 MW | Operational |

| Kadana | Gujarat | 240 MW | Not operating (vibration issues since 2004) |

| Ghatgar | Maharashtra | 250 MW | Operational |

| Bhira | Maharashtra | 150 MW | First private PSP in India |

Notable: Of approximately 4.7 GW installed, not all is operational in pumping mode. Sardar Sarovar (1,200 MW) lacks an operational lower reservoir. Kadana (240 MW) has been out of pumping service since 2004 due to vibration problems. Actual operational pumped storage capacity may be closer to 2.5-3.0 GW.

Under Construction (approximately 10-12 GW)

| Project | State | Capacity | Developer | Target |

|---|---|---|---|---|

| Tehri PSP | Uttarakhand | 1,000 MW | THDC | 3 units commissioned 2025 |

| Pinnapuram | Andhra Pradesh | 1,680 MW | Greenko | Unit 1 wet commissioning achieved |

| Kundah | Tamil Nadu | 500 MW | TANGEDCO/MEIL | Under construction |

| Turga | West Bengal | 1,000 MW | WBSEDCL | Target 2028 |

| Koyna Left Bank | Maharashtra | 80 MW | MKVDC | Delayed 12 years, 473% cost overrun |

Allocated by States (51 GW across 39 projects by 2032)

The major allocations:

| Developer | Planned Capacity | Key States |

|---|---|---|

| Greenko | 13.2 GW | Andhra Pradesh, Rajasthan |

| Adani Green | 11.4 GW | Andhra Pradesh, Uttar Pradesh |

| JSW Energy | 7.7 GW | Uttar Pradesh, Chhattisgarh |

| NHPC | 12.4 GW | Maharashtra, Andhra Pradesh |

| SJVN | 2.4+ GW | Mizoram, Maharashtra |

| Torrent Power | TBD | Gujarat, Maharashtra |

In Environmental Clearance Pipeline (154.9 GW across 131 projects)

The Ministry of Environment, Forest and Climate Change has issued 124 Terms of Reference and 9 Environmental Clearances for PSP since 2013. Seventy percent of these were issued after FY 2022-23, reflecting the recent acceleration.

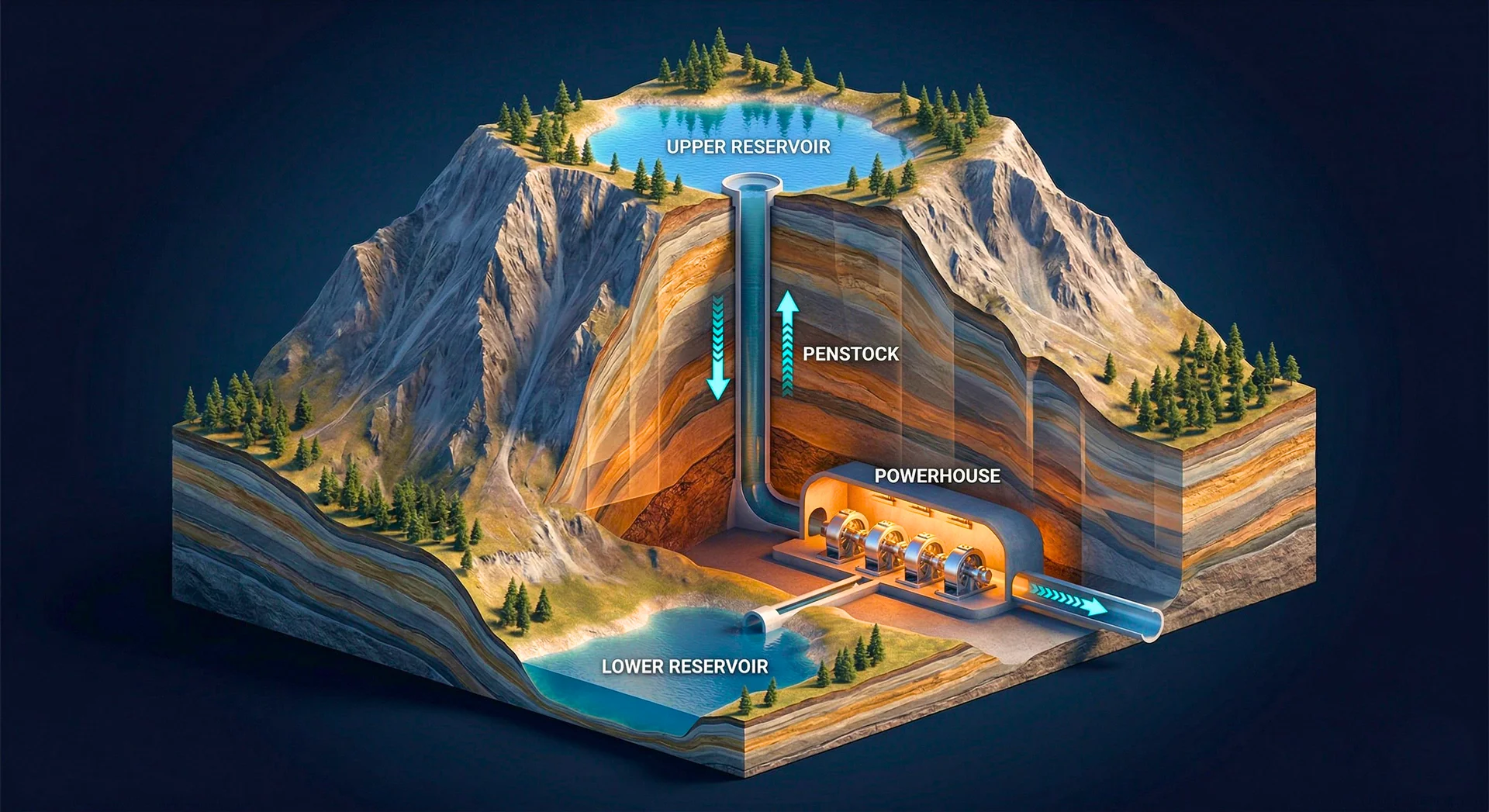

The Concrete Demand

Each pumped storage project requires:

- Upper reservoir dam (new construction in most closed-loop projects)

- Lower reservoir dam (new construction in closed-loop, or modifications to existing reservoir)

- Underground powerhouse cavern (the largest underground concrete structures in Indian infrastructure)

- Headrace and tailrace tunnels (with concrete or shotcrete lining)

- Surge shafts (large-diameter concrete-lined vertical shafts)

- Penstocks (steel-lined concrete tunnels)

- Access tunnels and adits (shotcrete-lined)

- Reservoir lining (concrete or asphalt concrete for upper reservoirs)

- Ancillary structures (switchyard, transformer cavern, cable tunnel, ventilation shaft)

For a 1,000 MW project like Tehri PSP, the concrete scope includes:

- Underground machine hall: 203 x 28.2 x 56 metres

- Two concrete-lined headrace tunnels: 8.5 m diameter, 930 and 1,060 m long

- Upstream surge shafts: 20.92 m diameter, 145 m high

- Downstream surge shafts: 19.5 m diameter, 70 m high

- Tailrace tunnels: 9.0 m diameter, 1,151 and 1,255 m long

Multiply this by 39 projects, and the cumulative concrete demand runs into tens of millions of cubic metres over the next decade.

The Readiness Question

Mix Design Capability

Pumped storage concrete includes mass concrete for dams (low heat, high SCM), HPC for spillways and flow channels (high strength, abrasion resistant), self-compacting concrete for complex underground geometry, shotcrete for tunnel and cavern support, and potentially RCC for gravity dams where speed is critical.

Each concrete type requires a different mix design, different materials, and different QC protocols. A single project may use 10-15 distinct mix designs across its structural elements.

The question: Does India have enough experienced concrete technology professionals to design and manage this many mix designs across 39 simultaneous projects?

Thermal Control Expertise

Every mass concrete dam in the pipeline requires a thermal control plan: thermal modelling, pre-cooling system design, placement scheduling, post-cooling design (for thick sections), and thermal instrumentation. These are specialised skills that require both analytical capability and field experience.

The question: India builds conventional hydropower dams sequentially, with a limited pool of thermal control specialists moving from project to project. Can this pool scale to serve dozens of simultaneous projects?

Quality Control Systems

Each project requires on-site testing laboratories, trained QC personnel, instrumentation and monitoring systems, and a documentation and reporting framework. The QC requirements for pumped storage concrete are more demanding than conventional hydropower because of the cyclic loading, cavitation, and reversible flow conditions.

The question: Where will the trained QC engineers, lab technicians, and concrete specialists come from? India’s engineering education system produces structural engineers, not concrete technology specialists.

Material Supply Chains

The projects need cement (including specialty types), fly ash or GGBS, silica fume, aggregates, admixtures, steel fibres, formwork, and pre-cooling/post-cooling equipment. Many of the planned sites are remote, with limited road access and long supply lines.

The question: Can the material supply chain for concrete (particularly SCMs and specialty admixtures) scale to support dozens of major projects simultaneously, many in remote locations?

What the History Tells Us

India’s track record with hydropower concrete is instructive:

Subansiri Lower: Cost overrun from Rs 6,285 crore to Rs 26,075 crore (4x). Delays of over a decade.

Koyna Left Bank PSP: 80 MW project delayed 12 years with 473% cost overrun.

Tehri PSP: Cost escalated from Rs 1,657.60 crore to Rs 4,825.60 crore.

24 of 37 hydropower projects under construction were delayed as of 2020, with cost overruns exceeding Rs 30,000 crore collectively.

These overruns have complex causes: geological surprises, environmental clearance delays, contractual disputes, funding gaps. But concrete technology problems are a recurring contributor: thermal cracking requiring repair, foundation treatment exceeding estimates, quality issues requiring rework, and schedule delays from placement problems.

The 51 GW pipeline will face these same challenges, at 10-20 times the scale.

What Needs to Happen

1. Concrete Technology as a Project-Level Discipline

Currently, concrete technology on Indian dam projects is often a subset of the structural design or the contractor’s construction management. It needs to be a standalone discipline with its own project-level leadership: a concrete technology consultant or team responsible for mix design, thermal control, QC systems, and material supply from pre-tender through commissioning.

2. Workforce Development

India needs a pipeline of concrete technology professionals with dam-specific expertise. This requires university curriculum development (concrete technology as a specialisation within civil engineering), industry training programmes (hands-on experience in thermal control, NDT, and grouting), and knowledge transfer from experienced professionals to the next generation.

3. Standards Modernisation

The inclusion of RCC and HPC chapters in the IS 456:2025 draft is a start. But India still lacks a modern mass concrete construction standard (IS 457 is from 1957), codified pumped storage concrete guidelines, and standardised QC protocols for the specific demands of PSH structures.

4. Material Supply Chain Investment

Fly ash supply will tighten as coal plants retire. GGBS supply is tied to steel production. Calcined clay (LC3) production is nascent. Silica fume is mostly imported. The pumped storage buildout needs a parallel investment in cementitious material production and distribution infrastructure.

5. Institutional Knowledge Capture

The lessons from Tehri PSP (self-compacting concrete for complex geometry, squeezing ground management), Purulia PSP (rockfill dam construction for PSH), and the early operational experience from Nagarjuna Sagar and Kadamparai need to be documented and disseminated. Currently, this knowledge resides with individual engineers and organisations.

The Opportunity

India’s pumped storage pipeline represents the largest sustained demand for dam concrete engineering in the country’s history. For concrete technology professionals, consulting firms, contractors, and material suppliers, this is a generational market opportunity.

But it is also a generational responsibility. The concrete placed in these projects will operate for 50-100 years, cycling daily, under conditions more demanding than any conventional dam. If the concrete technology is right, these projects will anchor India’s energy transition for decades. If it is wrong, they will join the list of Indian infrastructure projects defined by delays, overruns, and underperformance.

The policy framework is in place. The investment commitments are real. The renewable energy integration need is urgent. The question is whether the concrete technology capability will be ready when the first foundation pour begins.

That readiness starts with the decisions being made now: the mix designs being developed, the thermal control plans being written, the QC systems being specified, and the professionals being trained. The dam that performs for its 100-year design life is the one where the concrete technology was right from day one. Not from day one thousand.